If you have any sick leave, please email a copy of the sick note to payroll@notjustnumbersltd.co.uk, and confirm the first full day of sickness and also the actual return to work date, if the employee has now returned to work.

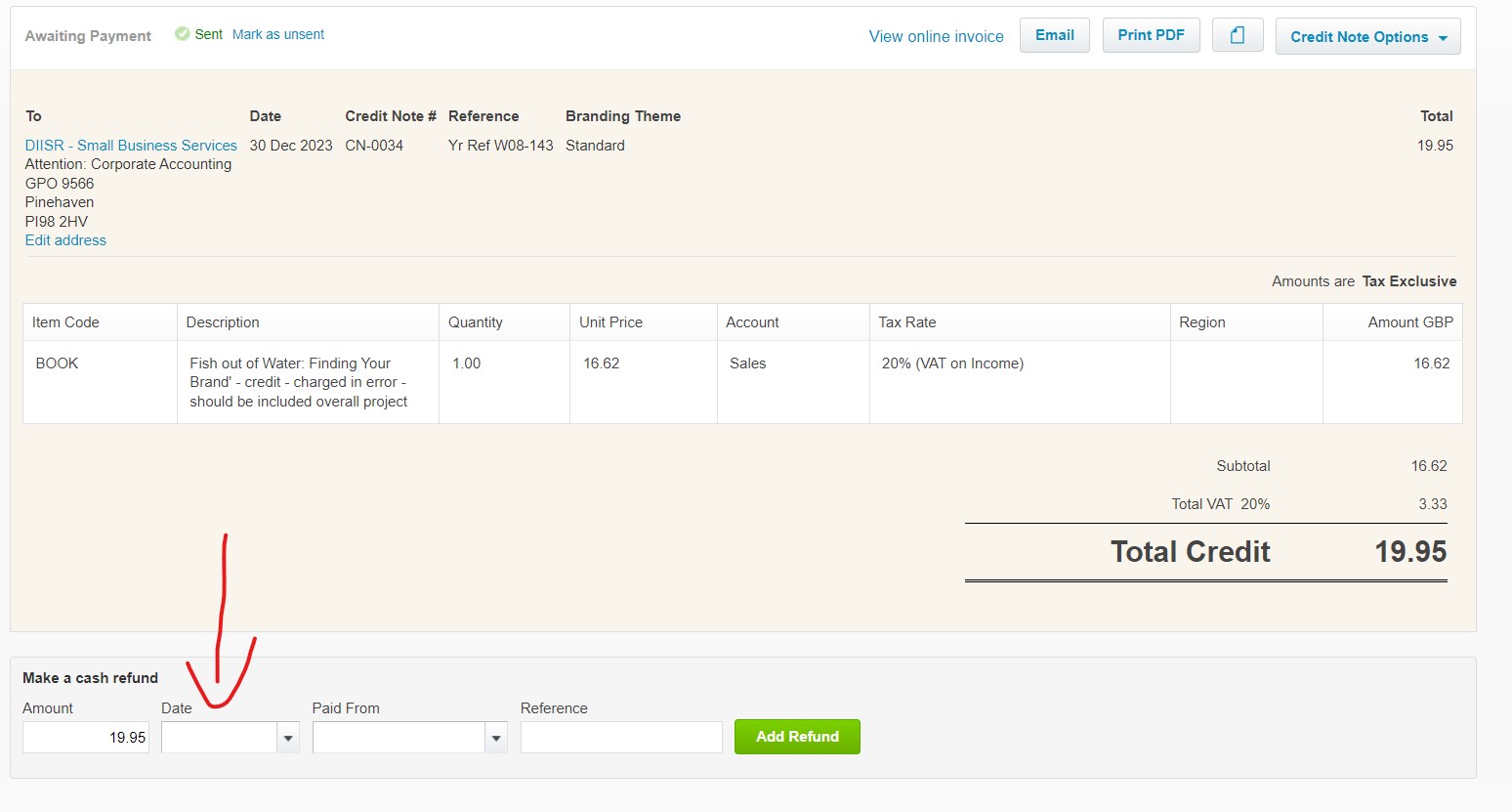

Overpayments and credit notes both need to be paid off to the bank accounts for them to appear in the bank reconciliation.

To do this go into either bills to pay or invoices, click into the credit note to open it up and complete the bottom line of the screenshot below. Enter the date it was refunded and enter the bank account it was paid to in the “paid from” section, then click add refund.

Office Equipment is used for Fixed Assets only (as are all the 700 account codes in Xero).

To be classed as a fixed asset it firstly has to be over a certain value (usually over £100.00 for small companies) and secondly it has to be a tool for your job. There are other factors but those are the main two. If you need help or clarification on where to code something in Xero, please do ask.

Unfortunately glitches do sometimes occur in the bank feeds which occasionally result in duplicated transactions or missed items so it is always a good idea to check that the balance in Xero matches the actual statement every month.

‘Trivial’ benefits are those that:

You can’t receive trivial benefits worth more than £300 in a tax year if you’re the director of a ‘close’ company.

A close company is a limited company that’s run by 5 or fewer shareholders.

Remember that ‘Trivial’ benefits in kind provided to employees and directors do not need to be reported on form P11d.

During the COVID pandemic the government relaxed the conditions to enable those working from home to be paid £6 a week tax free by their employer, or, where that was not paid by the employer, they could claim relief for £6 a week against their employment income for a tax refund from HMRC. Those relaxed rules applied for 2020/21 and 2021/22. Many employers and employees may not be aware that from 6 April 2022 the rules reverted to the strict statutory position. Employees can claim tax relief if they have to work from home under a homeworking agreement, for example because:

Tax relief cannot be claimed if the employee chooses to work from home.

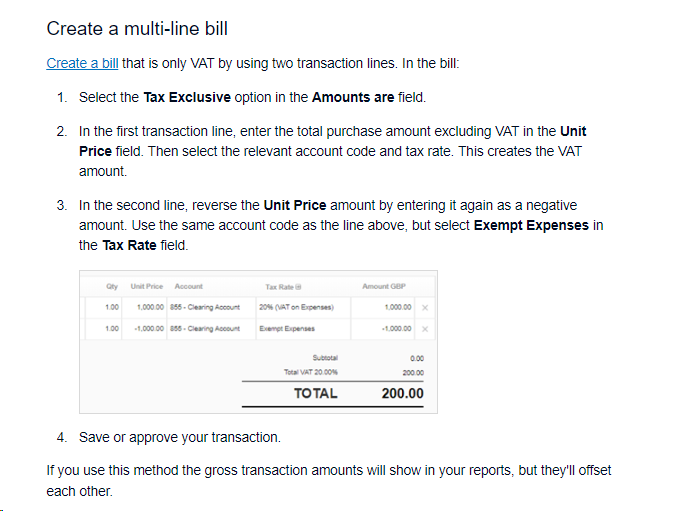

When recording your transactions within Xero it is important to make the distinction between zero rated items and exempt items for VAT purposes. Although neither will have VAT charged on them they are treated very differently for the purpose of the VAT calculation. Not using the correct rate will mean that the figure declared for the value of the purchases (box 7 on your VAT return) will not be accurate.

Goods and services which are categorised as 0% or zero-rated VAT are still taxable goods, but the rate of VAT charged is 0%.

Goods and services that fall into the zero-rated VAT category include:

Goods and services that fall into the exempt VAT category include:

The benefits all depend on the type of finance (and it gets more complex by the week as dealerships bring out new products!) so to keep it simple –

Lease rental – probably the cheapest way of doing it but you don’t own the car. You will put your lease payments through each month and get Corporation Tax relief on the payments. You will be able to claim 50% of the VAT on the lease payments and if you take a maintenance deal, then 100% VAT of the cost of that each month is claimable on that part. You hand the car back at the end of the term and get a new one.

Lease Purchase (Business PCP) – this is where it gets trickier! The bigger the balloon payment at the end the more HMRC think you will never own it so if you go down this road, keep the balloon payment smaller which will make It more expensive per month, but as with buying the car on Hire Purchase, the car will belong to you at the end of the term so you can offset 100% of the cost of the car against Corporation Tax in year 1. The car will sit on your balance sheet as an asset and the finance outstanding will show as a liability.

Hire Purchase – same tax rules as Lease Purchase but the monthly payments are much higher as you don’t get the balloon payment.

On top of that, the car has to be brand new.

There will be a benefit in kind which must be reported before July each year on a P11d benefits and expenses form. The benefit on a 100% electric car (not hybrid) is currently 2% of list price so if the car is say £40k list price (not what you pay for it but the manufacturers list price) then the benefit in kind would be £800 – so 20% tax on that would be £160 per annum. The company will then have to pay Class 1A National Insurance at 13.8% = £110.40 by 22nd July each year.

You can buy a charging point via the company too and get capital allowances on it.

The best way of claiming for charging is to claim the 9p (as at 1st March 2024) per business mile back from the company. All other running costs and insurance will be paid from the business.

A balance Sheet is a snapshot of your assets and liabilities on a given date. If you are a limited company then you’ll need to include a balance sheet in the accounts you have to submit annually to Companies House and HMRC.

A balance sheet has two sides that equal each other. One side is the total of your assets minus your liabilities. The other is the equity (shares) in the business plus the profits it has earned up to the balance sheet date.

Quite simply, no. Cash flow is only a way of recording the movement of money. Your business could be making a loss even if it has a positive cash flow. For example, a bank loan boosts your cash flow with extra funds but not your profit. Profit is what’s left after deducting your expenses from your revenue. Business expenses can include things you don’t actually pay for, like the depreciation of assets.

Ten tips to improve cashflow:

Always invoice customers as soon as a job is complete. Set out your payment terms, encourage customers to pay early, such as half up front, think about letting customers pay in instalments, offer discounts for prompt payment. Consider conducting credit checks on customers – this could help you avoid bad debts from unpaid bills.

Your suppliers’ payment terms may be flexible and it is always worth asking. You might be able to negotiate terms that better suit your cash flow. Check whether suppliers offer payments on account, for example, where you settle your outstanding bills at the end of each month.

Try and strip out unnecessary expenses, i.e. try using less electricity for lighting or cutting water consumption Driving more efficiently reduces fuel bills and extends the life of vehicles.

If you have employees, one way to improve cash flow is to review working patterns. Flexible working hours and rotas can help you spread staff costs. If you pay commissions or bonuses to staff, think about restructuring these to support your cashflow.

Review your pricing structure, especially if your costs have risen. A negative cash flow shows that your expenses are higher than your income – it might be because you aren’t charging enough. Look at areas like your markup on materials and profit margin to see if they need adjusting. Charging more is often the most successful method of how to improve cash flow

Too much stock sitting on shelves or in a warehouse is wasted money until it is used. Think about ‘just in time’ stock replenishment, where you only buy stock when you actually need it. Beware of supply delivery delays as they could force you to make more expensive last-minute stock purchases. Buying frequently used stock when you have funds, and before you need it, is a tried and tested way to control your small business cashflow.

Capital expenditures for assets like equipment, tools and vehicles can be a drain on cash flow The cost of ‘big ticket’ items can be spread over several years by leasing assets Hire purchase contracts also spread the cost and you will still own the asset at the end of the contract.

Invoice factoring is where you sell your unpaid sales invoices to a company that collects the money. Your business then receives money due on your invoices direct from the factoring company, although you’ll be charged a commission for doing this. Invoice factoring could be a great way to remove the hassle of chasing payments.

Forecasting when you expect to receive money and pay bills improves cash flow. Identify your sales trends, seasonality for example. Forecasting helps to plan for months when you receive less income. Look at your upcoming expenses and patterns of spending – this can make it easier to have money ready when the bills come in.

A positive cash flow means you could have surplus money waiting to be used. Put any spare money to work in savings accounts for your business Look at transferring funds to deposit accounts that pay interest, the interest you earn improves your cash flow.